Good afternoon!

For the latest updates from ICT in the insurance industry follow us on

LinkedIn and don’t forget to enable notifications 🔔

Find more Texas related P&C insurance information and news on the ICT website

|

TDI Publishes 2024 Biennial Report

|

TDI published its 2024 Biennial Report to the 89th Texas Legislature. TDI hosted a "Meet the Regulator" event on December 3, where Commissioner Cassie Brown delivered opening remarks and staff presented these recommendations. That was followed by an opportunity to engage with TDI's Property & Casualty division staff. ICT attended the event.

As a reminder, statute requires that TDI submit a report before each regular session with recommended changes in state laws relating to the regulation of the insurance industry or other areas under the agency's jurisdiction. The 2024 report contains three recommendations to the legislature and two "emerging issues", one which impacts property and casualty insurance. Below are some highlights from the report.

Recommendations

-

Require companies to tell consumers why their policy was declined, canceled, or nonrenewed - TDI recommends amending Insurance Code 551.002, 551.109, and 551.055 to require all companies to disclose the reasons for declining a policy application or why an existing policy was canceled or nonrenewed. TDI notes that most consumers are not aware they can request this information and that this requirement would increase transparency. The Texas Insurance Code already mandates disclosure for cancellations and non-renewals of commercial policies, but not declinations. TDI notes this would create consistency between personal and commercial lines and ensure clear and uniform requirements.

-

Align fire investigator salaries with other licensed peace officers - TDI recommends adjusting State Fire Marshal’s Office investigator salaries to match those of other licensed peace officers. This change aims to address hiring challenges and turnover by ensuring fair compensation for their law enforcement duties.

-

Improve Fraud Unit’s ability to investigate electronic communications -TDI recommends amending the Texas Code of Criminal Procedure to grant Fraud Unit investigators authority to access electronic data, allowing them the same legal authority as other state agencies' peace officers. Fraud Unit investigations often involve electronic communications, but without authority to access customer data, investigators must rely on other agencies, slowing the process.

Emerging Issue of Interest - Price and availability in the

homeowners and personal auto markets

The report highlights significant nationwide challenges in the homeowners and personal auto insurance markets, driven by factors such as more frequent severe weather events, rising inflation in goods and labor, and increasing reinsurance costs. It notes that, in Texas, while storms remain the leading cause of home insurance claims, escalating inflation and reinsurance expenses have further amplified the cost of property repairs and replacements.

Below are statistics from the report:

-

In Texas, in 2023, auto rates increased on average by about 25.5% and homeowners rates increased on average by about 21.1%.

-

A consumer’s bill, or premium, also reflects the value of the property they’re insuring. And home and vehicle values have gone up significantly. Between 2019 and 2023, median home prices in Texas rose by about 40% according to the Texas Comptroller’s Office, while the average cost of a new vehicle nationwide increased 30% according to Kelley Blue Book. All this new value needs coverage, which results in bigger bills for consumers.

-

Driver behavior is a contributing factor for auto insurance. In 2023, there were 559,000 vehicle collisions in Texas, causing 250,000 injuries and over 4,200 fatalities according to the Texas Department of Transportation.

The report outlines mitigation as an opportunity for the Legislature to contain insurance costs, or incentive programs related to constructing homes and roofs to more resilient standards able to better handle severe Texas weather. In relation to mitigation, they point to the Windstorm Market Incentives study conducted by Texas A&M at Galveston. The study can be found here.

|

ICT Submits Comments on Proposed Rule Prohibiting Tying

|

ICT submitted comments to the TDI on December 5, regarding its informal draft rule that seeks to prohibit certain tying practices as a new unfair trade practice under Chapter 541 of the Insurance Code. The comments emphasized that there is no statutory prohibition against tying in Chapter 541 and raised concerns about TDI's legal authority to adopt such a rule without explicit legislative authorization.

|

DWC Accepts Comments on Telemedicine Rule

|

DWC is accepting public comments on a proposed rule amending 28 Texas Administrative Code Section 133.30, concerning telemedicine, telehealth, and teledentistry services.

The amendments are necessary to allow treating doctors to perform maximum medical improvement examinations by telemedicine or telehealth when there is no impairment.

Learn more on the TDI website (PDF).

|

ICT & TDI Host Joint Committee on Insurance Fraud Tackles Emerging Trends and Legislative Updates

|

Texas Joint Committee on Insurance Fraud

Tackles Emerging Trends and Legislative Updates

The Texas Joint Committee on Insurance Fraud gathered key stakeholders to discuss issues, trends, and strategies to combat insurance fraud in Texas. Jointly hosted by the Insurance Council of Texas (ICT) and the Texas Department of Insurance (TDI), the Dec. 3, 2024, meeting featured experts on recent cases, prosecution strategies, fraud prevention, and legislative updates. Highlights included updates from the TDI Fraud Unit, the Division of Workers’ Compensation, and national perspectives from the Coalition Against Insurance Fraud and the National Insurance Crime Bureau. The session concluded with a legislative update from ICT’s Jon Schnautz, who discussed bills that could impact the industry and efforts by ICT and other trade groups to ensure a competitive and robust insurance market in Texas. The committee fosters collaboration to protect Texans and uphold the integrity of the insurance system.

|

|

ICT in the News: Some consumers learn they'd have to bundle to keep their insurance policy

|

Homeowners in Texas, particularly in the Houston area, face soaring insurance premiums due to high risk from hurricanes and other extreme weather. Texas saw an average 23% rate increase in 2023, making it the third most expensive state for home insurance. Rich Johnson, public affairs representative for the Insurance Council of Texas, advises consumers to shop around annually, consider bundling policies, and explore discounts to reduce costs.

Key Points:

- Texas Premiums Rising: Texas experienced a 23% average increase in homeowners insurance premiums in 2023, the highest in the nation, according to S&P Global.

- Shop Around Annually: Rich Johnson of ICT recommends comparing policies yearly to find the best rates, as insurers calculate premiums differently.

- Consider Bundling Policies: Bundling homeowners and auto insurance can lower premiums since it spreads risk for insurers, especially in high-risk areas.

- Adjust Your Deductible: Increasing deductibles may lower premiums, but homeowners should ensure they can afford out-of-pocket costs during a claim.

- Explore Discounts: Discounts may apply for security systems, newer roofs, or memberships in affiliated organizations, so consumers should ask their insurers about available savings.

|

|

ICT in the News: Some consumers learn they'd have to bundle to keep their insurance policy

|

A North Texas homeowner alleges her insurance company required her to bundle home and auto insurance to renew her policy, sparking debate over consumer rights. The Texas Department of Insurance (TDI) reported similar complaints this year, prompting a draft rule to prohibit such requirements. Rich Johnson, spokesperson for the Insurance Council of Texas, emphasized that consumers can shop for alternatives in Texas’ competitive insurance market.

Key Points:

- Bundling Requirements: Some insurers, like Farmers, have reportedly required policyholders to bundle home and auto insurance to renew coverage.

- Regulatory Action: TDI is reviewing a draft rule that could ban bundling requirements as a condition for policy renewal or issuance.

- Consumer Guidance: Homeowners are advised to act quickly upon nonrenewal notices, shop for competitive quotes, and compare coverage details carefully.

- Market Context: Insurance companies cite rising claims and losses due to storms as drivers of underwriting changes and increased rates.

- ICT's Stance: Rich Johnson of ICT highlighted the competitive options available in Texas and noted that insurers manage risks based on market conditions.

|

|

Blaming insurance companies for high premiums is too easy, lowering them is hard.

|

Commentary/Houston Chronicle & San Antonio Express News

|

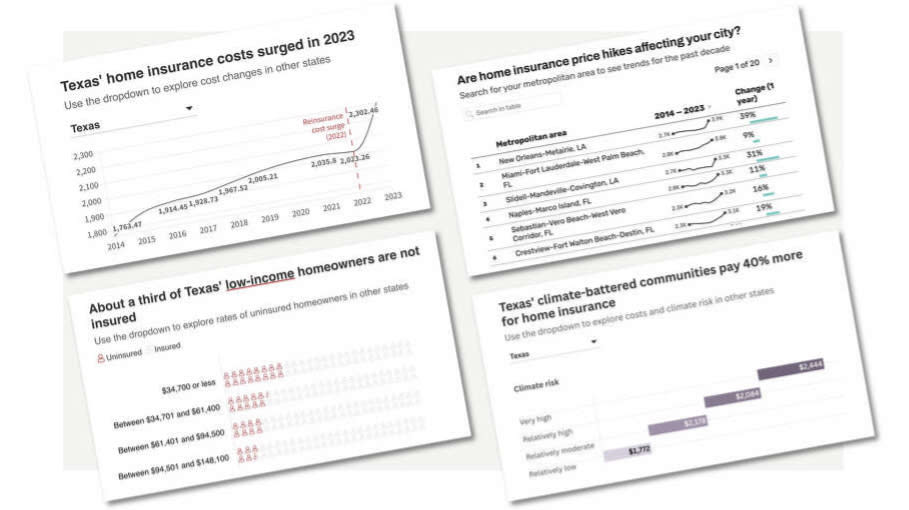

Texas homeowners are grappling with surging insurance premiums, which rose 21% statewide in the past year, driven by rising climate-related disasters and costly rebuilding practices. Average premiums now exceed $2,300 annually, leaving nearly a third of low-income homeowners without coverage. Experts emphasize that reducing premiums requires addressing the underlying risks, such as extreme weather, unsustainable rebuilding, and climate change.

Key Points:

- Premium Increases: Texas homeowners saw an average premium jump to $2,302 in 2023, compared to $1,763 in 2014, adjusted for inflation.

- Inequitable Risk Sharing: Insurance pools spread risks statewide, causing residents in safer areas to subsidize rebuilding in disaster-prone zones.

- Climate Change Impacts: Human-induced climate change is intensifying hurricanes, wildfires, and other extreme weather, driving up claims and premiums.

- Unsustainable Practices: Policies allowing repeated rebuilding in high-risk areas inflate costs for all policyholders.

- Solutions Needed: Lowering premiums requires reducing disaster risks through resilient construction, emissions cuts, and stricter rebuilding standards.

|

|

Houston Chronicle Runs Series of Stories on Challenges for Homeowners Insurance in Texas

|

The Houston Chronicle has launched a series examining Texas' escalating homeowners insurance crisis, which has been fueled by a rise in extreme weather events such as hurricanes and hailstorms. Texas ranks as the third most expensive state for home insurance, with premiums skyrocketing and many residents opting out of coverage altogether. The series explores how these costs impact Texans, why rates have surged, and what solutions state lawmakers may consider when they reconvene in January.

Key Points:

- Soaring Insurance Costs: Texas homeowners face some of the nation’s highest insurance premiums, with a statewide average increase of 21% in 2023, double the 2022 rate hike.

- Broad Impact Beyond Coasts: While coastal areas face rising premiums due to hurricane risks, inland regions are also grappling with higher rates from extreme storms and temperature changes.

- Residents Opting Out: Rising costs have forced some Texans to forgo insurance altogether, leaving them vulnerable in the event of a disaster.

- Carrier Responses: Insurance providers have avoided pulling out of Texas but have raised premiums and dropped coverage in high-risk areas to mitigate financial losses.

- Legislative Focus: The Chronicle's investigation aims to highlight potential solutions lawmakers could adopt during the 2025 legislative session to address the crisis.

|

|

Net written premium up 8.5%, underwriting profit $4.1B in Q3

|

The U.S. property/casualty insurance industry reported an $8.5% increase in net premiums written, totaling $691.2 billion for the first nine months of 2024, and netted a $4.1 billion underwriting profit, reversing a $32.1 billion loss in the same period of 2023, according to A.M. Best Co. Net income doubled to $130 billion, driven by a 22.1% rise in investment income. The industry's combined ratio improved to 97.9%, with catastrophe losses accounting for 8.8 points, down from 10.0 in 2023.

Key Points:

- Premium Growth: Net premiums written increased 8.5% to $691.2 billion for the first nine months of 2024.

- Improved Profitability: The industry recorded a $4.1 billion underwriting profit, compared to a $32.1 billion loss in 2023, and net income doubled to $130 billion.

- Combined Ratio: The combined ratio improved to 97.9% from 103.7% in the same period last year, with reduced catastrophe losses contributing to the improvement.

- Investment Income Surge: Net investment income rose 22.1% to $60.5 billion.

- Industry Surplus Growth: Policyholder surplus increased by 6.2%, reaching $1.017 trillion, reflecting financial stability.

|

|

Hurricanes, severe thunderstorms and floods drive insured losses above USD 100 billion for 5th consecutive year

|

Hurricanes, severe thunderstorms, and floods have driven insured losses above $100 billion for the fifth consecutive year, according to the Swiss Re Institute’s 2024 report. The U.S. was the hardest-hit, with Hurricanes Helene and Milton causing $50 billion in losses, while Europe and the Middle East saw major floods amounting to $13 billion. As climate change intensifies extreme weather, insured losses are expected to continue rising, with adaptation and mitigation measures becoming increasingly critical.

Key Points:

- Insured Losses: Estimated global insured losses for 2024 are set to exceed $135 billion, with the U.S. suffering the largest share.

- Hurricanes: Hurricanes Helene and Milton caused approximately $50 billion in insured losses in the U.S.

- Flooding: Europe and the UAE experienced severe floods, resulting in nearly $13 billion in insured losses, marking the second costliest year for floods in Europe.

- Climate Change Impact: The rising frequency and intensity of natural disasters are linked to climate change, emphasizing the need for mitigation and adaptation strategies.

- Urban Risk: Economic development and urban sprawl in high-risk areas are increasing insured losses, making flood protection measures like dykes and dams critical for future resilience.

|

Check out all things ICT!

|

|

Litigation Costs Drive Claims Inflation

|

Join us for an insightful webinar with Martin Boerlin of SwissRe - Explore the complex forces driving claims inflation in the U.S. commercial casualty insurance sector. Over the past five years, losses surged by 11% annually, reaching $143 billion in 2023—33% more than global natural catastrophe insured losses. Martin Boerlin will delve into social inflation, the societal trends and legal dynamics fueling skyrocketing liability claim costs. Discover how factors like large verdicts, litigation funding, and emerging risks impact insurers and businesses. Gain insight into SwissRe's groundbreaking social inflation index, the implications of these trends internationally, and strategies for navigating this challenging landscape.

Register here

|

The Insurance Council of Texas (ICT) is on the lookout for knowledgeable and engaging speakers for our 2025 events! We are looking for experts to discuss industry trends at our upcoming gatherings, including:

- Quarterly ICT Webinar Series

- Workers' Comp Conference: September 15-16, 2025

- P&C Insurance Symposium: September 17-18, 2025, in Austin, TX

We’re seeking speakers to cover critical industry trends, topics such as:

- Emerging topics and innovations

- Legal developments affecting insurance

- AI and technology: challenges and opportunities

- Resiliency strategies for businesses and communities

- Insights on the future of the insurance industry

If you have suggested topics, would like to request a speaker or would like to present at one of ICT's events, click here to let us know.

|

Enjoying this newsletter? Feel free to share it with your colleagues! Just a reminder: The ICT News to Know is a benefit exclusive to ICT members and we ask you not share outside your organization.

|

This email was sent on behalf of Insurance Council of Texas, 5508 W US Hwy 290, Ste 100, Austin, TX 78735. To unsubscribe click here.

If you have questions or comments concerning this email contact Insurance Council of Texas at webmaster@insurancecouncil.org.

|

|